Overview

In 2024, Reunion facilitated a $200M transfer of §45 production tax credits (PTCs) between two large publicly traded companies. The deal, involving credits from over 100 wind and utility-scale solar facilities spanning 10+ sites, marked a first-time transaction in federal clean energy tax credits for this Fortune 500 buyer.

Reunion addressed both the buyer’s desire to minimize out-of-pocket expenses and the seller's objective to maximize cashflow by structuring terms that included quarterly arrears payments and a capped true-up mechanism to account for production variability. Furthermore, audit readiness was a key requirement for the buyer. This was solved by developing a dynamic, audit-friendly, and reusable data room that houses robust due diligence documentation. This successful transaction laid the foundation for future deals between the parties including a "repeat" 2025 transaction.

The Deal Highlights

§45

PTC

Credit type

$200M - $220M

Volume

Quarterly true-ups

100+

Facilities

Wind & Utility Solar

Energy Community

Bonus Adder

On a subset of assets

Aligning Buyer and Seller Motivations

Matching transaction needs, deal-worthiness criteria, and cash flow considerations across buyer and seller was essential to hatching the deal.

The Buyer

Fortune 500

Corporation

with operations throughout the U.S.

Ownership: Publicly Traded

Deal lead: Director of Tax

Transactional experience: First time purchasing §6418 clean energy tax credits.

Motivations

Minimize out-of-pocket expenses by paying for credits quarterly on estimated tax payment dates

Purchase from a single, experienced counterparty, ideally publicly traded, who can provide $200M+ of credits

Minimize transactional risk by purchasing PTCs that are exempt from PWA requirements

The Seller

Diversified Energy

Company

with over 2GW in operation across the U.S.

Ownership: Publicly Traded

Deal lead: VP of Tax

Transactional experience: Prior experience with tax equity and transferability.

Motivations

Maximize cashflow by monetizing quarterly and garnering a compelling price

Sell to a single counterparty who is capable of purchasing $200M-220M of PTCs

Partner with a Fortune 500 buyer with consistent annual tax liability and potential for repeat transaction

Negotiating terms for mutual success

Managing cash flow timing and production uncertainty ensured a predictable, flexible and successful transfer.

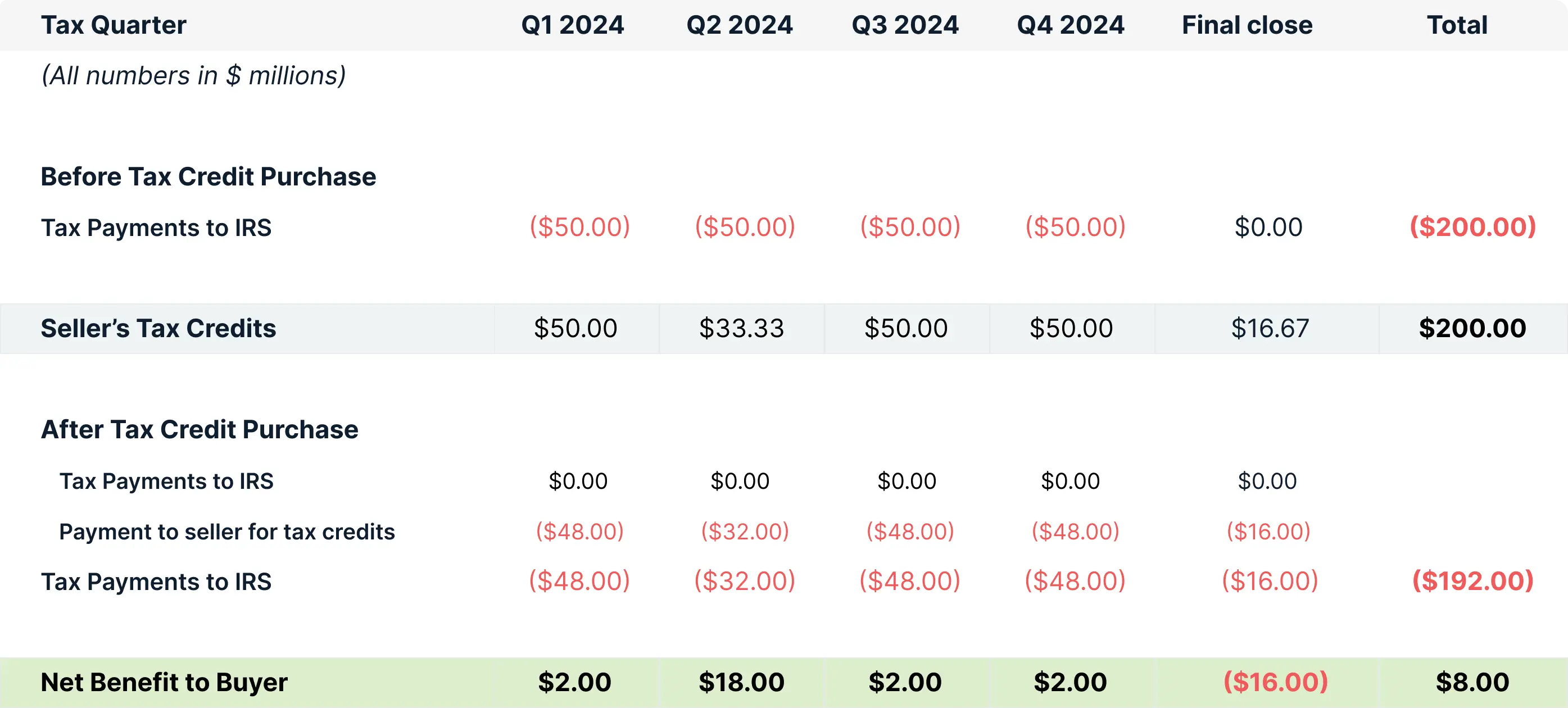

Minimizing out-of-pocket expenses

Reunion structured credit payments quarterly in arrears, on or after the buyer’s estimated tax payment date, avoiding the need to go out-of-pocket when compared to regular tax payments.

$200M

Credit Cap

Up to $220M

Mutual option to increase cap

True Ups

Scheduled quarterly + year end, subject to cap

Addressing PTC Uncertainity

Flexible terms were created to account for variability in production figures (commonly adjusted for up to six months after generation) and mid-year publication of PTC rates, both of which can impact the PTC volume generated.

Thoroughly but efficiently mitigating risk

Employing unique approaches to facilitate a thorough but efficient due diligence process.

Tax credit qualification

Validated tax credit qualification for 100+ energy facilities across 4 Regional Transmission Organizations (RTOs) by mapping them onto recent satellite images to confirm their existence, location, and function.

PTC Rates & PWA Requirements

Consolidated disparate files onto a single dashboard to confirm relevant Placement In Service (PIS) and Beginning Of Construction (BOC) dates. and as such determine PTC credit rates and exemptions from Prevailing Wage and Apprenticeship (PWA) requirements.

Energy generation & sale

Substantiated the generation and sale of electricity to third parties by aggregating settlement files from four RTOs that corresponded to the relevant facilities and creating a software tool to validate the amount of electricity sold.

Achieving an audit-ready posture

Helping the buyer, who is currently in the Compliance Assurance Process (CAP), become “audit-ready” with detailed documentation for possible IRS Information Document Requests (IDRs).

1

Aggregated industry knowledge regarding previous IDRs

...for wind and solar projects. Reunion relied extensively on tax equity audits as precedent, given the nacency of tax credit transfers under §6418.

2

Built a robust data room with all books, records, and documentary evidence

...that would need to be readily available, including documents that otherwise may not have been included in diligence.

3

Documented the diligence process and data room contents in a memo

...that summarizes key information about the tax credit seller and the complete tax credit portfolio.

Built a robust data room with all books, records, and documentary evidence

...that would need to be readily available, including documents that otherwise may not have been included in diligence.

1

2

3

Aggregated industry knowledge regarding previous IDRs

...for wind and solar projects. Reunion relied extensively on tax equity audits as precedent, given the nacency of tax credit transfers under §6418.

Documented the diligence process and data room contents in a memo

...that summarizes key information about the tax credit seller and the complete tax credit portfolio.

Spotlight: Maintaining a live data room

Given the “audit-ready” nature of this transaction, Reunion maintains a dynamic data room for the buyer and seller.

Risk categories

Date room contents (not exhaustive)

Seller diligence

Seller diligence

Organizational chart and other ownership documents

Financial statements

Qualification

Qualification

Satellite imagery + exhaustive collection of site control documents

Interconnection documents

Numerous XML files from multiple grid operators reflecting energy settled/sold

PTC amount

PTC amount

Documentary evidence for PIS dates: Turbine completion certificates, EPC substantial completion certificates, correspondence regarding permission to operate between interconnection parties

Documentary evidence for BOC dates: BOC certificates, memorandums documenting safe harbor strategies employed (Physical Work Test and Five Percent Test), relevant supporting evidence, including supply and product agreements, bank statements, invoices, purchase orders and bills of lading, construction progress imagery from third party site visits, etc.

Repower documentation (“80/20” test)

PWA and bonus credits

PWA and bonus credits

Documentation of prevailing wage exemptions due to placement-in-service dates or beginning of construction dates, as diligenced above under “Amount of PTC”

Turbine by turbine location verification (latitude and longitude coordinates) to confirm energy community eligibility

Final Reflections

This §45 PTC transfer is a perfect example of how a thoughtful, well-structured transaction can add lasting value to the buyer and the seller.

Diligence presented challenges because of the “audit-ready” standard, and the size of the portfolio with over 100 facilities across 10+ sites.

However, due to the nature of PTC transactions, the majority of diligence is reusable for additional PTC transfers from this portfolio in subsequent calendar years.

Both parties will be able to use the original due diligence package for repeat deals by leveraging materially similar deal terms and the same portfolio of projects. Supplemental diligence will be focused around any changes to the portfolio, and validation of production and sale of electricity in 2025.

As of the publication of this case study, the buyer and seller have in fact executed a “repeat” 2025 transaction.

Get your deal done with the industry-leading team that has facilitated >$5B in tax credits transfers since 2024

.webp)